A slim white pouch tucked under the lip. No smoke, no tobacco leaf, yet it delivers a hit of nicotine that rivals a cigarette. This simple product description has sent regulators, legal experts, and industry leaders into a decade‑defining debate: what exactly is a nicotine pouch?

The answer is anything but academic. Depending on whether a jurisdiction labels the pouch a tobacco product, a medicine, or a general consumer good, an entirely different set of rules kicks in — governing everything from taxation and advertising to where the product can be sold and who can buy it. As the global market races toward a projected $19.5 billion valuation by 2028, the battle over classification has become the single most consequential regulatory front.

This article unpacks the three competing frameworks, maps how different countries are drawing their lines, and explains why the outcome of this debate will shape the next era of the nicotine industry.

Why Classification Is Everything

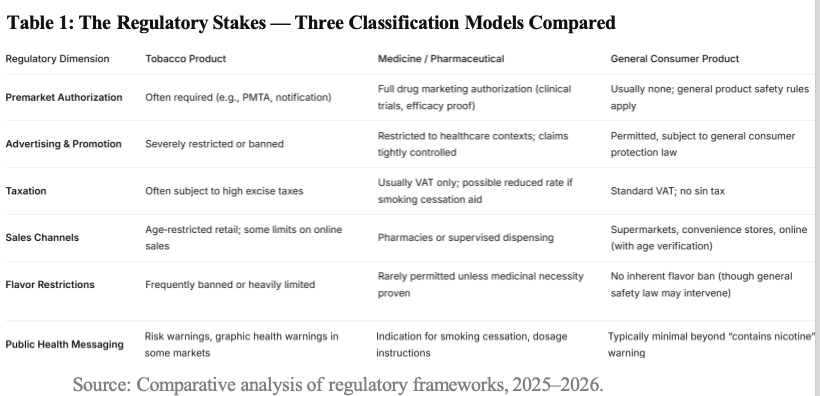

Classification is not merely a labeling exercise. It is the regulatory key that unlocks — or locks — the market. The table below illustrates how drastically the commercial reality changes under each framework.

Table 1: The Regulatory Stakes — Three Classification Models Compared

The table makes clear that classification is a proxy for market access and profitability. For manufacturers, being deemed a “consumer good” is the most favorable commercial environment, while “medicine” represents the most restrictive — yet also the only route that officially allows claims about helping smokers quit.

The Three Frameworks in Practice

1. Tobacco Product: Regulated by Association

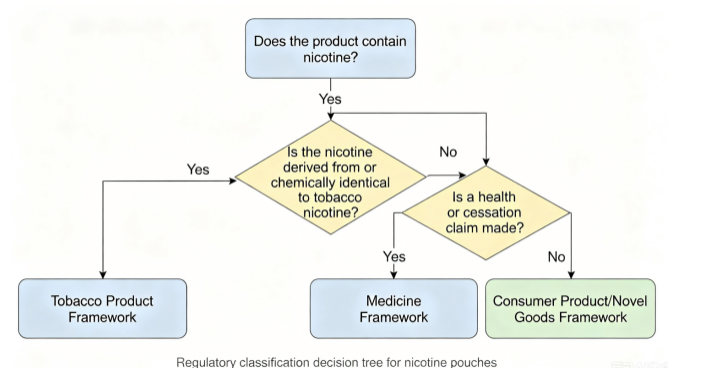

This is the most common fallback position. Because nicotine pouches deliver nicotine — historically derived from tobacco, even if now often synthesized — many countries have simply absorbed them under existing tobacco control legislation. The United States, through the FDA’s Center for Tobacco Products, and the European Union member states that classify them under the Tobacco Products Directive (or national tobacco laws) are prime examples.

The logic is straightforward: nicotine is the defining addictive and toxicological agent of tobacco, and any nicotine‑containing product that is not a proven medicine ought to be caught by the tobacco net. The consequence is that pouches face the same battery of restrictions as cigarettes: excise tax, marketing bans, plain packaging potentials, and rigorous premarket scrutiny.

2. Medicine: A High Bar with a Clear Purpose

If a nicotine pouch is marketed as a smoking cessation aid or as a product that “treats, prevents, or cures nicotine dependence,” it crosses into pharmaceutical territory. This triggers the most demanding regulatory pathway: clinical trials, good manufacturing practice (GMP) certifications, and marketing authorization akin to that required for nicotine patches or gums.

The UK’s Medicines and Healthcare products Regulatory Agency (MHRA) has explicitly indicated that nicotine pouches making cessation claims would require medicinal licensing. Similarly, Canada’s classification of nicotine pouches as natural health products — a quasi‑medical framework — mandates an authorization that includes evidence of safety, efficacy, and quality.

Very few manufacturers have chosen this route voluntarily. However, the medicinal classification remains a powerful policy tool for governments that want to restrict access to “recreational” nicotine pouches while keeping a door open for therapeutic use. The debate in several Asian and Middle Eastern countries is moving in precisely this direction.

3. General Consumer Product: The Grey Zone Gamble

In some markets, the absence of tobacco leaf has led to nicotine pouches falling into a regulatory vacuum — being sold as a general consumer good, often subject only to basic product safety regulations and age‑verification at the point of sale. This has been the de facto situation in countries like Germany (until recent legislative proposals), much of Eastern Europe, and parts of Latin America.

From a public health perspective, this approach is fiercely contested. Opponents argue that treating a potent nicotine delivery system as a simple commodity normalizes addiction and risks a new wave of youth uptake — with minimal oversight on ingredients, nicotine strength, or marketing. Proponents counter that over‑regulating a product that is significantly less harmful than smoking could drive users back to cigarettes.

The European Commission has been monitoring this fragmentation and is expected to propose a dedicated “novel nicotine product” category in the next Tobacco Products Directive revision, potentially ending the consumer‑product grey zone for the entire bloc.

A World Divided: Current Classification Landscape

The map of regulation is, for now, a patchwork. The table below captures how key markets classify nicotine pouches as of mid‑2026.

Table 2: Nicotine Pouch Classification by Market (2026 Snapshot)

The Consequences of Classification Chaos

For global manufacturers, the patchwork is an operational headache. A product legally sold in a Swedish supermarket cannot be shipped across the border to Finland without facing tobacco excise, and the same brand may need entirely different packaging, labeling, and marketing strategies in the US versus the UK.

This fragmentation also complicates the public health conversation. Without a shared regulatory language, it is harder to collect consistent safety data, harmonize warning labels, or enforce age‑gate compliance across platforms. The World Health Organization’s Framework Convention on Tobacco Control (WHO FCTC) has begun preliminary discussions on whether oral nicotine products require a dedicated protocol, but consensus remains distant.

Where the Debate Is Heading

Three trajectories are becoming visible for the next five years:

·The Separate Framework Model (Sweden’s blueprint): A growing number of countries are concluding that nicotine pouches are neither tobacco nor medicine, but a distinct category requiring tailor‑made rules. This allows governments to set nicotine limits, ban youth‑appealing flavors, and levy moderate taxation without forcing the product into the cigarette regulatory box.

·The Medicinal Gateway: For jurisdictions deeply opposed to recreational nicotine use, the medicinal route offers a way to ban broad consumer access while still allowing smokers a medically supervised transition aid. Australia and, to some extent, Canada are early adopters of this philosophy.

·Full Tobacco Integration: The simplest legislative path is to bring pouches fully under tobacco law — an approach favored by countries with strong anti‑tobacco lobbies and limited appetite for legislative innovation. The risk here is that taxing nicotine pouches like cigarettes could make them less accessible than far more harmful smoked products, undermining harm reduction.

Conclusion

The question “Is it a tobacco product, a medicine, or a consumer good?” is not a semantic riddle. It is the axis on which public health strategy, industry viability, and consumer safety will turn. As nicotine pouches move from niche to mainstream, the window for coherent, evidence‑based classification is narrowing. The countries that build a dedicated, proportionate framework now may well define the global standard — while those that default to borrowed categories may find themselves fighting regulatory fires for years to come.

For regulators, the challenge is to avoid the mistakes of the e‑cigarette era, where fragmented rules and reactionary bans often deepened the market chaos. For the industry, the message is equally clear: proactively engaging with the classification debate — backed by robust science and a genuine commitment to preventing youth access — is no longer optional. It is the only path to a stable, sustainable market.