1. Overall Market Size of the Global Next-Generation Tobacco Industry

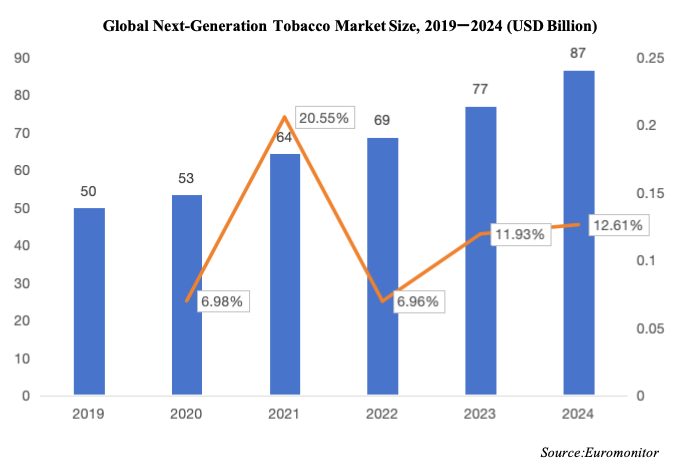

According to data published by Euromonitor, the global next-generation tobacco market maintained steady growth from 2019 to 2024, with an average annual growth rate of approximately 14%, reflecting rapid market expansion.

In 2023, the global next-generation tobacco market reached approximately USD 76.9 billion, representing a year-on-year increase of 11.93%. In 2024, the market size further expanded to around USD 86.6 billion, up 12.61% compared with the previous year. From 2019 to 2024, the compound annual growth rate (CAGR) reached 11.70%.

This trend highlights the continuously increasing global demand for next-generation tobacco products.

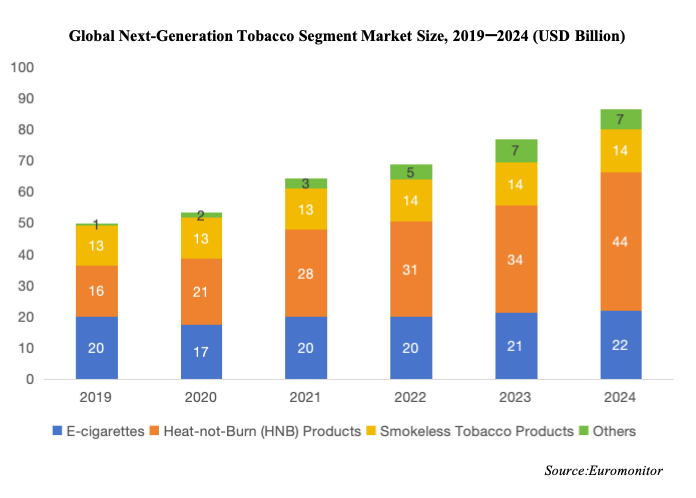

1.1 Market Size of Global Next-Generation Tobacco Segments

The global e-cigarette market has continued to grow steadily. In 2023, the global e-cigarette market size reached USD 21.2 billion, up 6.84% year-on-year. Preliminary estimates indicate that the market size reached approximately USD 21.9 billion in 2024.

The three major segments of the next-generation tobacco industry — e-cigarettes, heated tobacco products (HTPs), and smokeless tobacco products — recorded the following market sizes:

2.Analysis of Global E-Cigarette Market Development

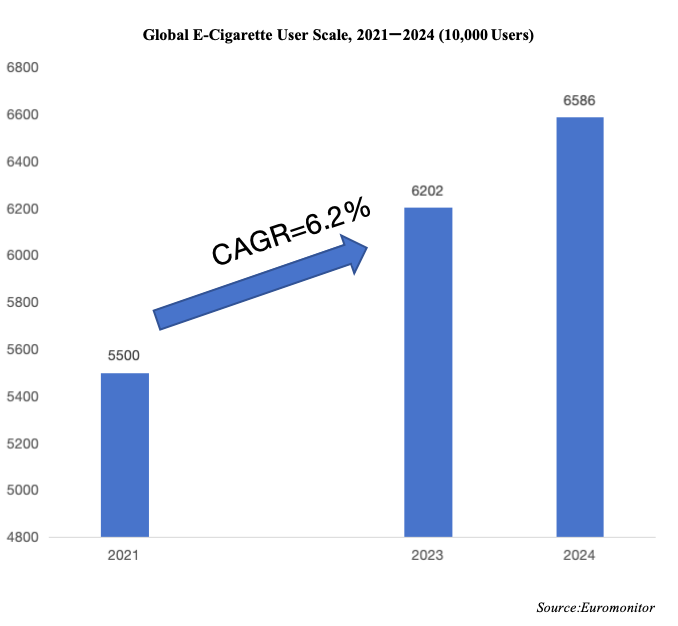

2.1 Global E-Cigarette User Base

According to data disclosed by Euromonitor, the number of global e-cigarette users increased by more than 7 million between 2021 and 2023, with the total consumer base surpassing 62 million in 2023. Preliminary estimates suggest that the global e-cigarette user base reached 65.86 million in 2024.

2.2 Global E-Cigarette Market Segmentation

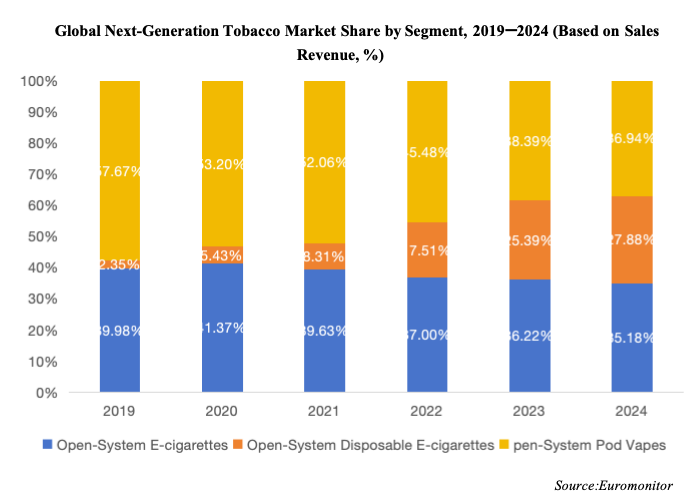

From 2019 to 2024, open-system e-cigarettes consistently maintained a market share above 30% in the global e-cigarette market, although their share gradually declined from nearly 40% to around 35%.

Meanwhile, closed-system e-cigarettes steadily expanded their market share, increasing from approximately 60% to nearly 65%. However, significant structural changes occurred within the closed-system category itself: disposable e-cigarettes rapidly gained market share, while pod-based systems continued to decline, with their share dropping from nearly 58% in 2019 to approximately 37% in 2024.

Within the closed-system market, disposable e-cigarettes have increasingly displaced pod-based products. This shift is largely driven by disposables’ price advantage, convenient user experience, and broad flavor variety, which have rapidly reshaped the market landscape. Disposable products require no separate device purchase, offer lower usage costs, and deliver higher puff counts per unit, allowing them to expand quickly amid rising economic pressures.

At the same time, regulatory restrictions on flavored pod-based products have positioned disposables as a “legal alternative” for flavor diversity, attracting a significant migration of users. On the brand side, fast-moving consumer goods (FMCG)-style strategies — including frequent product launches and diverse packaging designs — have further stimulated repurchase behavior among younger consumers, strengthening market stickiness and accelerating the marginalization of pod-based systems.

By contrast, pod-based e-cigarettes are facing dual pressure from regulation and shifting market structures. On one hand, increasingly strict environmental policies in Europe and North America are pushing companies to adopt recyclable and circular product designs, while pod-based products have been relatively slow to adapt. On the other hand, in markets where flavor restrictions and compliance costs continue to rise, many consumers are turning to illicit flavored products or directly switching to disposable devices, resulting in significant user loss for pod-based systems.

More fundamentally, pod systems have lagged behind in product innovation, user experience upgrades, and regulatory adaptation. As consumer preferences evolve, these products are gradually being overshadowed by disposable devices that offer clearer positioning and lighter operational models.