Oral nicotine products are primarily consumed by adult smokers and individuals seeking to quit smoking. These products offer a smoke-free experience that significantly reduces exposure to harmful chemicals, while delivering moderate nicotine release through the oral mucosa.

According to the World Health Organization (WHO), there were 1.245 billion adult tobacco users globally in 2022. Data from British American Tobacco (BAT) indicates that by 2024, there were approximately 16 million oral nicotine users worldwide — representing just 1.3% market penetration, compared with 5.3% for e-cigarettes. This suggests substantial room for growth in the oral nicotine category.

Driven by increasing global health awareness and stricter smoking restrictions, demand for oral nicotine products continues to grow. As smoke-free and ignition-free alternatives, they appeal to consumers seeking safer and more convenient options. Their versatility — suitable for indoor, public, or social use — makes them even more adaptable than traditional cigarettes or e-cigarettes

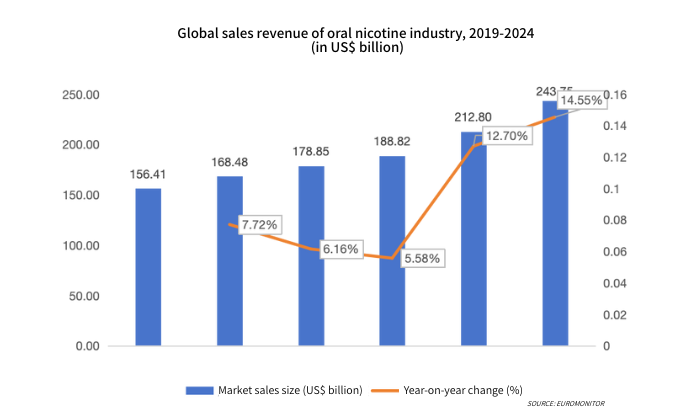

From 2019 to 2024, the global oral nicotine market maintained strong momentum, reaching USD 24.38 billion in 2024, up 14.55% year-on-year. Analysts project continued double-digit growth as nicotine pouch adoption accelerates worldwide.

Between 2019 and 2024, the global oral nicotine industry experienced a major structural transition — from traditional smokeless tobacco (snus, chewing tobacco) to modern nicotine pouches.

While smokeless tobacco products continue to decline due to health concerns and regulatory pressure, tobacco-free nicotine pouches have surged in popularity. Their flexible legal status, diverse flavors, and adjustable nicotine strengths appeal to a wider audience. Leading tobacco companies such as BAT (VELO), Swedish Match (ZYN), and NIIN are heavily investing in production, branding, and marketing to expand their pouch portfolios.

By 2024, nicotine pouches accounted for 44.88% of the global oral nicotine market, up from 4.85% in 2019, overtaking traditional snus (50.57%) and chewing tobacco (4.55%).

From 2019 to 2024, global snus sales volume fell from 76,690 tons to 68,867 tons, declining over 1,500 tons annually. Key reasons include:

Growing health awareness among consumers

Strict regulation classifying snus as a tobacco product

Competition from e-cigarettes and nicotine pouches

Chewing tobacco sales fluctuated mildly between 45,000–47,000 tons during 2019–2024. The category remains stable in regions like the U.S., Sweden, and India, supported by older consumers with traditional habits.

Between 2019 and 2024, global nicotine pouch sales skyrocketed from 1.76 billion to 21.24 billion units, achieving a compound annual growth rate (CAGR) of 64.57% — the fastest among all new nicotine categories.

Growth drivers include:

Regulatory flexibility: Unclear legal classification allows smoother market entry.

Corporate expansion: Global campaigns by BAT (VELO) and Swedish Match (ZYN).

Product advantage: Multiple flavors and nicotine strengths compared to restricted e-liquids.

The global oral nicotine market is entering a period of accelerated transformation. As tobacco-free innovation reshapes consumer habits, nicotine pouches have emerged as the dominant format, bridging harm reduction and convenience. For industry stakeholders, this category represents not only commercial growth but also a step toward a more sustainable and responsible nicotine future.